NAIC Consumer Rep Blasts Proposed Changes to Pet Insurance Model Law To Be Discussed June 7

After six-months of sidelining the Pet Insurance Model Law aimed at protecting consumers – and following what has been an almost three-year drafting process— the National Association of Insurance Commissioners (NAIC) Pet Insurance Working Group will meet again on June 7 to consider proposed changes to the model law.

NAIC Consumer Representative Birny Birnbaum, who is also the Executive Director of the Center for Economic Justice, called the proposed changes to the draft “stunning” in an email to TCR last week.

“The proposal before the [NAIC Pet Insurance Working Group] is stunning — what was pitched as a minor tweak is now a wholesale removal of any required producer training for a product that is significantly different from other products sold by p/c producers.”

In insurance parlance, “producer” refers to insurance companies, and what Birnbaum is objecting to is, in essence, is an elimination of training and licensing requirements for those selling pet insurance.

Trupanion: “Our own employees receive training over and above….”

Not everyone apparently believes more requirements imposed by insurance regulators are likely to make pet insurance a more consumer-friendly, attractive product. Trupanion, for example, when asked about Birnbaum’s statement, took the position that their “own employees receive many hours of training over and above what is required to obtain their Property & Casualty insurance licenses,” Trupanion spokesman Michael Nank wrote in part to TCR in a statement on producer licensing requirements:

“Trupanion supports informed and appropriately-trained people selling our products. Our own employees receive many hours of training over and above what is required to obtain their Property & Casualty insurance licenses. We also believe that the appropriate level of training will vary. For example, in our view a person who already holds a license to sell a life or health policy should not need the same training as someone with no insurance background. It is important to note that if a state chooses to allow someone who does not hold a Property & Casualty license to sell our industry’s products, it may also impose its own training requirement regardless of the wording in the Model Law.”

Nationwide’s representative on the Working Group, Dr. Jules Benson, declined to comment on Birnbaum’s reaction to the proposed changes through spokeswoman Karen Davis. Nationwide, the leading provider of pet insurance in the U.S. with more than 1,000,000 active policy holders, also declined to weigh in on Trupanion’s position.

Removing requirements or punting to states?

In our earlier reporting, (NAIC) spokesperson Stephanie Bryant identified producer licensing as the most significant remaining issue the group had yet to address as of December 2020. “There was a lot of discussion on the licensing section,” Bryant wrote in an email, pointing to comments offered in the sub-sections of the law from various states, along with stakeholders such as Trupanion, the American Veterinary Medical Association (AVMA), and NAPHIA.

For a while, it seemed that the licensing issue had been punted to a different committee and out of the Pet Insurance Working Group. It now seems that the licensing issue has been punted once again, with the changes proposed in the latest draft effectively leaving the issue to individual states. Given the state of play with the legislation Maine was able to sign into law on April 7, which requires fully licensed producers, punting the issue to states does not appear to have made the regulatory environment less stringent. The first state to pass NAIC legislation, after all, did so with the producer licensing requirements.

Here are the proposed changes to Section 7 of the draft model, which pertain to training and licensing. Note all the deletions:

PET INSURANCE MODEL ACT

Section 1.Short Title

This Act shall be known as the “Pet Insurance Act.”

Section 2.Scope and Purpose

A.The purpose of this Act is to promote the public welfare by creating a comprehensive legal framework within which Pet Insurance may be sold in this state.

B.The requirements of this Act shall apply to Pet Insurance policies that are issued to any resident ofthis state, and are sold, solicited, negotiated, or offered in this state, and policies or certificates thatare delivered or issued for delivery in this state.

C.All other applicable provisions of this state’s insurance laws shall continue to apply to PetInsurance except that the specific provisions of this Act shall supersede any general provisions of law that would otherwise be applicable to Pet Insurance.

Section 3.Definitions

If a pet insurer uses any of the terms in this Act in a policy of pet insurance, the pet insurer shall use the definition of each of those terms as set forth herein and include the definition of the term(s) in the policy. The pet insurer shall also make thedefinition available through a clear and conspicuous link on the main page of the pet insurer or pet insurer’s program administrator’s website.

Nothing in this Act shall in any way prohibit or limit the types of exclusions pet insurers may use in their policies or require pet insurers to have any of the limitations or exclusions defined below.

As used in this Act:

- “Chronic condition” means a condition that can be treated or managed, but not cured.

- “Congenital anomaly or disorder” means a condition that is present from birth, whether inherited or causedby the environment, which may cause or contribute to illness or disease.

C.“Hereditary disorder” means an abnormality that is genetically transmitted from parent to offspring and may cause illness or disease.

D.“Pet insurance” means a property insurance policy that provides coverage for accidents and illnesses of pets.

Drafting Note: The description of this line as “property” is only for purposes of financial reporting of data.

E.“Preexisting condition” means any condition for which any of the following are true prior to the effective date of a pet insurance policy or during any waiting period:

(1) A veterinarian provided medical advice;

(2) The pet received previous treatment; or

(3) Based on information from verifiable sources, the pet had signs or symptoms directly related to the condition for which a claim is being made.

A condition for which coverage is afforded on a policy cannot be considered a preexisting condition on any renewal of the policy.

F.“Veterinarian” means an individual who holds a valid license to practice veterinary medicine from the appropriate licensing entity in the jurisdiction in which he or she practices.

G.“Veterinary expenses” means the costs associated with medical advice, diagnosis, care, or treatment provided by a veterinarian, including, but not limited to, the cost of drugs prescribed by a veterinarian.

H.“Waiting period” means the period of time specified in a pet insurance policy that is required to transpire before some or all of the coverage in the policy can begin. Waiting periods may not be applied to renewals of existing coverage.

I.“Renewal” means to issue and deliver at the end of an insurance policy period a policy which supersedes a policy previously issued and delivered by the same pet insurer or affiliated pet insurer and which provides types and limits of coverage substantially similar to those contained in the policy being superseded.

J.“Orthopedic” refers to conditions affecting the bones, skeletal muscle, cartilage, tendons, ligaments, and joints. It includes, but is not limited to, elbow dysplasia, hip dysplasia, intervertebral disc degeneration, patellar luxation, and ruptured cranial cruciate ligaments. It does not include cancers or metabolic, hemopoietic, or autoimmune diseases.

K.“Wellness program” means a subscription or reimbursement-based program that is separate from an insurance policy that provides goods and services to promote the general health, safety, or wellbeing of the pet. If any wellness program [insert language from state statute or regulation that defines the trigger for insurance contracts, which might include language such as: [undertakes to indemnify another], or [pays a specified amount upon determinable contingencies] or [provides coverage for a fortuitous event]], it is transacting in the business of insurance and is subject to the insurance code. This definition is not intended to classify a contract directly between a service provider and a pet owner that only involves the two parties as being “the business of insurance,” unless other indications of insurance also exist.

Section 4.Disclosures

- A pet insurer transacting pet insurance shall disclose the following to consumers:

(1) If the policy excludes coverage due to any of the following:

(a) A preexisting condition;

(b) A hereditary disorder;

(c) A congenital anomaly or disorder; or

(d) A chronic condition.

(2) If the policy includes any other exclusions, the following statement: “Other exclusions may apply. Please refer to the exclusions section of the policy for more information.”

(3) Any policy provision that limits coverage through a waiting or affiliation period, a deductible, coinsurance, or an annual or lifetime policy limit.

(4) Whether the pet insurer reduces coverage or increases premiums based on the insured’s claim history, the age of the covered pet or a change in the geographic location of the insured.

(5) If the underwriting company differs from the brand name used to market and sell the product.

B.Right to Examine and Return the Policy.

(1)Unless the insured has filed a claim under the pet insurance policy, pet insurance applicants shall have the right to examine and return the policy, certificate or rider to the company or an agent/insurance producer of the company within fifteen (15) days of its receipt and to have the premium refunded if, after examination of the policy, certificate or rider, the applicant is not satisfied for any reason,

(2)Pet insurance policies, certificates and riders shall have a notice prominently printed on the first page or attached thereto including specificinstructions to accomplish a return. The following free look statement or language substantially similar shall be included:

“You have 15 days from the day you receive this policy, certificate or rider to review it and return it to the company if you decide not to keep it. You do not have to tell the company why you are returning it. If you decide not to keep it, simply return it to the company at its administrative office or you may return it to the agent/insurance producer that you bought it from as long as you have not filed a claim. You must return it within 15 days of the day you first received it. The company will refund the full amount of any premium paid within 30 days after it receives the returned policy, certificate, or rider. The premium refund will be sent directly to the person who paid it. The policy, certificate or rider will be void as if it had never been issued.”

C.A pet insurer shall clearly disclose a summary description of the basis or formula on which the pet insurer determines claim payments under a pet insurance policy within the policy, prior to policy issuance and through a clear and conspicuous link on the main page of the pet insurer or pet insurer’s program administrator’s website.

D.A pet insurer that uses a benefit schedule to determine claim payment under a pet insurance policy shall do both of the following:

(1) Clearly disclose the applicable benefit schedule in the policy.

(2) Disclose all benefit schedules used by the pet insurer under its pet insurance policies through aclear and conspicuous link on the main page of the pet insurer or pet insurer’s program administrator’s website.

E.A pet insurer that determines claim payments under a pet insurance policy based on usual and customary fees, or any other reimbursement limitation based on prevailing veterinary service provider charges, shall do both of the following:

(1) Include a usual and customary fee limitation provision in the policy that clearly describes the pet insurer’s basis for determining usual and customary fees and how that basis is applied in calculating claim payments.

(2) Disclose the pet insurer’s basis for determining usual and customary fees through a clear and conspicuous link on the main page of the pet insurer or pet insurer’s program administrator’swebsite.

F.If any medical examination by a licensed veterinarian is required to effectuate coverage, the pet insurer shall clearly and conspicuously disclose the required aspects of the examination prior to purchase and disclose that examination documentation may result in a preexisting condition exclusion.

- Waiting periods and the requirements applicable to them, must be clearly and prominently disclosed to consumers prior to the policy purchase.

- The pet insurer shall include a summary of all policy provisions required in subsections (A) through (G), inclusive, in a separate document titled “Insurer Disclosure of Important Policy Provisions.”

- The pet insurer shall post the “Insurer Disclosure of Important Policy Provisions” document required in subsection (H) through a clear and conspicuous linkon the main page of the pet insurer or pet insurer’s program administrator’s website.

- In connection with the issuance of a new pet insurance policy, the pet insurer shall provide the consumer with a copy of the “Insurer Disclosure of Important Policy Provisions” document required pursuant to subsection (H) in at least 12-point type when it delivers the policy.

- At the time a pet insurance policy is issued or delivered to a policyholder, the pet insurer shall include a written disclosure with the following information, printed in 12-point boldface type:

(1)The [insert state insurance department]’s mailing address, toll-free telephone number andwebsite address.

(2)The address and customer service telephone number of the pet insurer or the agent or broker of record.

(3)If the policy was issued or delivered by an agent or broker, a statement advising the policyholder to contact the broker or agent for assistance.

- The disclosures required in this section shall be in addition to any other disclosure requirements required by law or regulation.

Section 5.Policy Conditions

A.A pet insurer may issue policies that exclude coverage on the basis of one or more preexisting conditions with appropriate disclosure to the consumer. The pet insurer has the burden of proving that the preexisting condition exclusion applies to the condition for which a claim is being made.

B.A pet insurer may issue policies that impose waiting periods upon effectuation of the policy that do not exceed 30 days for illnesses or orthopedic conditions not resulting from an accident. Waiting periods for accidents are prohibited.

(1)A pet insurer utilizing a waiting period permitted in Subsection 6B shall include a provision in its contract that allows the waiting periods to be waived upon completion of a medical examination. Pet insurers may require the examination to be conducted by a licensed veterinarian after the purchase of the policy.

(a)A medical examination under Subsection 6B(1) shall be paid for by the policyholder, unless the policy specifies that the pet insurer will pay for the examination.

(b)A pet insurer can specify elements to be included as part of the examination and require documentation thereof, provided the specifications do not unreasonably restrict a consumer’s ability to waive the waiting periods in section Subsection 6B.

(2)Waiting periods and the requirements applicable to them, must be clearly and prominently disclosed to consumers prior to the policy purchase.

C.A pet insurer must not require a veterinary examination of the covered pet for the insured to have their policy renewed.

D.If a pet insurer includes any prescriptive, wellness, or non-insurance benefits in the policy form, then it is made part of the policy contract and must follow all applicable laws and regulations in the insurance code.

E.An insured’s eligibility to purchase a pet insurance policy must not be based on participation, or lack of participation, in a separate wellness program.

Section 6.Sales Practices for Wellness Programs

- A pet insurer and/or producer shall not do the following:

(1) Market a wellness program as pet insurance;

(2) Market a wellness program during the sale, solicitation, or negotiation of pet insurance.

- If a wellness program is sold by a pet insurer and/or producer:

(3) The purchase of the wellness program shall not bea requirement to the purchase of pet insurance.

(4) The costs of the wellness program shall beseparate and identifiable from any pet insurance policy sold by a pet insurer and/or producer.

(5) The terms and conditions for the wellness program shall be separate from any pet insurancepolicy sold by a pet insurer and/or producer.

(6) The products or coverages available through thewellness program shall not duplicate products or coverages available through the pet insurance policy; and

(7) The advertising of the wellness program shall notbe misleading and shall be in accordance with Subsection 7B of this Model.

(8) A pet insurer and/or producer shall clearly disclose the following to consumers, printed in 12-point boldface type:

(a) That wellness programs are not insurance.

(b) The address and customer service telephone number of the pet insurer or producer or broker of record.

(c) The [insert state insurance department]’s mailing address, toll-free telephone number, and website address.

C.Coverages included in the pet insurance policy contract described as “wellness” benefits are insurance.

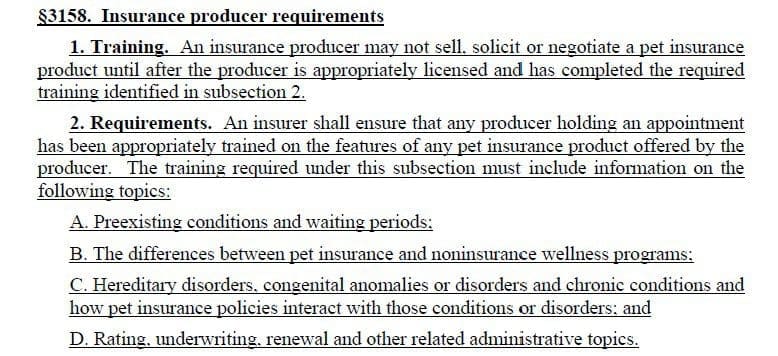

Section 7.Insurance Producer Training

- An insurance producer shall not sell, solicit, or negotiate a pet insurance product until after the producer is appropriately licensed and has completedthe requiredtraining identified in subsection B of this Section determined by this state to be necessary to sell this product.

- ProducerTraining RequirementsTraining for Insurance Producers with a Major Lines License.Insurer shall ensure that its producers have been appropriately trained on the features of its products.

Drafting Note: States may wish to include training requirements in this section to be required of producers licensed in their state to sell this product.

Drafting Note: The major line license referenced here is a reference to the Producer Licensing NAIC Model Act (#218). See Section 8E for the term “major line,” and Section 7A(1) through (6) for a listing of those major lines, or see the NAIC State Licensing Handbook, Chapter 9, Lines of Insurance, The Major Lines.

(1) Training for Limited Lines Producers

(a) A limited lines insurance producer shall not sell, solicit, or negotiate a pet insurance product until after the producer completes training courses approved by the department of insurance and provided by the department of insurance-approved education provider.

(b) The minimum length of the initial training required under this subsection shall be sufficient to qualify for at least ten (10) pre-licensing education or continuing education credit hours.

(c) In addition to the training required in Paragraphs (a) and (b) of this subsection, alimited lines insurance producer who sells, solicits, or negotiates pet insurance shall complete ongoing training as set forth in paragraph (d).

(d) The ongoing training required by this subsection shall be no less than four (4) continuing education credit hours prior to every license renewal.

(e) The training required under this subsection may also qualify for a state’s pre-licensing education or continuing education credit hours in accordance with [insert reference to state law or regulations governing producer continuing education course approval].

(f) Providers of pet insurance training that qualifies for pre-licensing or continuing education shall comply with the reporting requirements and shall issue certificates of completion in accordance with [insert reference to state law or regulations governing producer continuing education course approval].

(g) The satisfaction of the training requirements of another state that are substantially similar to the provisions of this section shall be deemed to satisfy the training requirements of this subsection in this state.

(h) The satisfaction of the components of the training requirements of any course or courses with components substantially similar to the provisions of this section shall be deemed to satisfy the training requirements of this subsection in this state.

(i) An insurer shall verify that a producer has completed the pet insurance training courses required under this section before allowing the limited lines producer to sell, solicit or negotiate pet insurance for that insurer. An insurer may satisfy its responsibility under this paragraph by obtaining certificates of completion of the training course or obtaining reports provided by commissioner-sponsored database systems or vendors or from a reasonably reliable commercial database vendor that has a reporting arrangement with approved insurance education providers.

Drafting Note: A state department of insurance may separately authorize a limited line producer to sell, solicit, or negotiate pet insurance, not based on authority in this statute. See Uniform Licensing Standards section 37 (Non-Core Limited Lines) and Chapter 9 of the Producer Licensing Handbook.

- The training required under this section shall include information on the following topics:

(1) Preexisting conditions and waiting periods;

(2) The differences between pet insurance and non-insurance wellness programs;

(3) Hereditary disorders, congenital anomalies or disorders, and chronic conditions and how pet insurance policies interact with those conditions; and

(4) Rating, underwriting, renewal, and other related administrative topics.

Section 8. Regulations

The commissioner may adopt reasonable rules and regulations, as are necessary to administer this part.

Section 9. Violations

Violations of this Act shall be subject to penalties pursuant to [insert state administrative code].